Understanding Minimum Essential Coverage (MEC) can be complicated when compared to minimum value, essential health benefits, and actuarial value.

Let’s start by answering: what is it and what does it cover? Minimum Essential Coverage is a plan that meets the Affordable Care Act (ACA) requirements for health coverage. Some of these programs include:

Marketplace plans

Job-based plans

Medicare

Medicaid

All applicable large employers (ALEs) with 50 or more full-time or full-time equivalent employees are required by law to provide ACA-compliant health coverage to their employees. ALEs who do not provide coverage ACA-compliant coverage are subject to fines and penalties from the Internal Revenue Service.

What Are the Minimum Essential Coverage Option Levels Available?

There are three different plan options available. Understanding the difference between the three helps employers decide which MEC plan is best for their employees.

Standard MEC plans are ACA compliant and include coverage for wellness, preventative services, prescription discounts, and telehealth services.

Enhanced MEC plans take coverage one step further than standard plans and are aimed at attracting and retaining top talent by also including primary and urgent care visits with low copays, and discounted specialist and laboratory services.

The highest-level MEC plans include the enhanced MEC plan benefits along with added coverage such as prescription coverage and low copays.

What Do Minimum Essential Coverage Plans with Hospital Indemnity Cover?

The goal of worksite MEC plans is to provide affordable healthcare coverage for the average person. MEC plans with added hospital indemnity policies can offset high deductibles and full out-of-pocket expenses so that an emergency does not become a financial crisis. The 10 health benefits they include are:

Ambulatory Patient Services (outpatient services)

Emergency Services

Hospital Visits

Maternity and Newborn Care

Pediatric Services (including oral and vision)

Mental Health and Substance Use Disorder Services (including behavioral health treatment)

Prescription Drugs

Rehabilitative and Habilitative Services and Devices

Laboratory Services

Preventative and Wellness Services and Chronic Disease Management

How Much Do You Save With MEC?

ALEs who fail to provide 95% of their full-time employees with ACA-compliant benefits are subject to high fines and penalties. Use our calculator to find out how much your business can save by providing Minimum Essential Coverage benefits while staying compliant with federal regulations.

Use our MEC Benefits calculator to see how much your business can save by offering MEC coverage.

What is the Difference Between MEC and Minimum Value?

Minimum value is a higher threshold than MEC. Minimum value is when a plan pays 60% of the actuarial value of allowed benefits under the plan. If a large employer offers benefits and meets Minimum Essential Coverage requirements, but they do not meet the minimum value, they meet the ACA employer requirements.

MEC and Essential Health Benefits

Essential health benefits are the core benefits that “qualified health plans” must cover. MEC also has a lower threshold than essential health benefits. If a group health plan doesn’t provide all of the benefits under essential health benefits, the coverage will likely meet Minimum Essential Coverage, so companies will be ACA-compliant.

Why is it Important to Understand the Differences?

Each of these coverage specifications is important to ensure large employers provide proper coverage to their employees. As an employer, you must understand your legal liability in providing benefits, as well as understanding what coverage you need to offer your employees to give them the best options and ensure compliance with the ACA.

Curious why offering health insurance to your employees is so important? It encourages and promotes a healthier, happier, and stronger workforce. Read our article that explains why healthy employees improve work productivity here.

https://innovativehia.com/wp-content/uploads/2022/12/iStock-1359838986-2.jpg13182275magdihttps://innovativehia.com/wp-content/uploads/2020/08/InnovativeHIA_logo2-1030x407.pngmagdi2024-03-25 19:21:312024-04-05 15:45:07What is MEC and What Does It Cover?

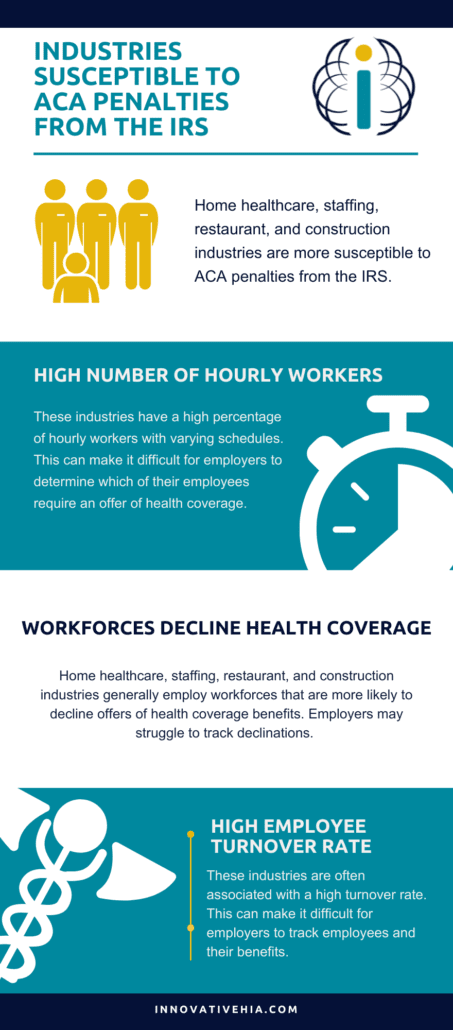

While all organizations are susceptible to receiving IRS penalties, some industries are particularly vulnerable. These industries include home healthcare, staffing, restaurant, and construction industries.

Why are these industries under fire from the IRS? Let’s take a look.

These Industries Typically Have a High Number of Hourly Workers

Home healthcare, staffing, restaurant, and construction industries have a high percentage ofhourly workers with varying schedules. This can make it difficult for employers to determine which employees are ACA full-time and require an offer of health coverage.

HR is often a non-centralized function, making it challenging to gather the data necessary for compliance.

High Staff Turnover Rates

These industries are often associated with a high employee turnover rate. This can make it difficult for employers to track employees as their benefits.

Workforces that Disproportionately Decline Health Coverage

Home healthcare, staffing, restaurant, and construction industries generally employ workforces that are more likely to decline offers of health coverage benefits. Employers may struggle to track declinations and face ACA penalties from the IRS.

How Can Organizations Ensure They Are Complying with ACA Requirements?

Employers can ensure they are ACA compliant by determining the accurate full-time and part-time status of employees under ACA. Employers may experience significant ramifications for misclassifying employees.

Additionally, employers should familiarize themselves with their requirements under the ACA’s Employer Mandate. For example, employers with 50 or more full-time employees, or ALEs, must:

“Offer Minimum Essential Coverage (MEC) to at least 95% of their full-time employees (and their dependents) whereby such coverage meets Minimum Value (MV); and

Ensure that the coverage for the full-time employee is affordable based on one of the IRS-approved methods for calculating affordability.”

For more information, read on for the full article from the ACA Times.

These Industries are Most at Risk for ACA Penalties From the IRS

The home healthcare, staffing, restaurant, and construction industries are under fire from the IRS for failing to comply with the ACA. Organizations within these industries have been shocked to receive ACA penalty notices from the IRS that are in the millions of dollars.

Of course, all types of organizations – hospitality, manufacturing municipal governments, non-profits, and other industries – are receiving IRS penalty notices too. However, the four industries mentioned above seem to be getting more than their fair share.

Here’s why these industries are so susceptible to receiving ACA penalties:

HR is often a non-centralized function, making it challenging to gather the data necessary for compliance

They have a high percentage ofhourly workers with varying schedules, making it difficult to determine who is ACA full-time and requires an offer of health coverage

They employ workforces that disproportionately decline offers of health coverage benefits, creating a heavier employer burden in tracking declinations

Employees come and go during the year with high staff turnover rates, increasing the employer’s burden to track all such employees

Per diem piece work and multiple rates of pay complicate the determination of pay rates and affordability

Reliance on payroll systems (or other software programs) that collate data and submitForms 1094-C and 1095-C often result in a failure to let you know when the data used is inaccurate, which will trigger ACA penalties

Determining the accurate full-time and part-time status of employees under the ACA is arguably the first, and most important, step for ACA compliance. There are real ramifications for inaccurately classifying employees.

Under the ACA’s Employer Mandate, ALEs, or employers with 50 or more full-time employees and full-time equivalent employees to:

Offer Minimum Essential Coverage (MEC) to at least 95% of their full-time employees (and their dependents) whereby such coverage meets Minimum Value (MV); and

Ensure that the coverage for the full-time employee is affordable based on one of the IRS-approved methods for calculating affordability

ALEs that fail to comply with these requirements can be subject to Internal Revenue Code (IRC) Section 4980H penalties.

For example, let’s look at an employer that improperly classifies an employee as not full-time and does not make an offer of insurance. That employee goes to a government marketplace exchange to purchase health insurance and receives a Premium Tax Credit (PTC) that helps subsidize the cost of the health insurance purchased on the exchange. This can trigger the issuance of an IRS Letter 226J penalty notice under IRC 4980H.

The penalty assessment will be applied to every full-time employee working for that employer during the course of the tax year, not just the employee obtaining the PTC. For the 2022 tax year, that penalty could be as high as $275,000 for every 100 employees.

The first step in the full-time status evaluation is determining which measurement method is best for your organization.

For organizations made up primarily of variable-hour employees, you will want to implement the Look-Back Measurement Method. If your workforce has mostly full-time employees and non-varying schedules, the Monthly Measurement Method will be best.

The most expedient step for employers is to get your ACA Vitals score. This will help determine your risk of receiving IRS penalties by analyzing your unique workforce composition.

Such a review can reap dividends by helping employers avoid significant ACA penalties from the IRS, particularly if those organizations have not been filing ACA-required information annually with the IRS. These organizations should file this information as soon as possible to avoid receiving an IRS penalty notice and to minimize potential penalties.

The IRS is currently issuing warning notices to employers identified as having failed to file and furnish Forms 1094-C and 1095-C for the 2019 tax year via Letter 5699. If you have received one, contact us to have the penalty reduced or eliminated. We’ve helped our clients prevent over $1 billion in ACA penalty assessments.

If you are part of the home healthcare, personnel staffing, restaurant and construction industries, or any industry that relies on a significant mix of full-time and part-time employees, you are at serious risk of being penalized for not complying with the ACA.

We see daily how the IRS is enhancing its methods for identifying employers that are not complying with the ACA and sending them penalty notices.

We regularly see the surprise and shock expressed by organizations that receive these penalty notices, many of them containing significant penalty assessments.

We also see how these organizations could have avoided these penalty assessments by receiving help from experts that understand ACA and IRS regulatory requirements and know how to successfully meet those regulatory requirements.

https://innovativehia.com/wp-content/uploads/2022/08/Which-Industries-are-Most-Susceptible-to-ACA-Penalties-from-the-IRS.png6281200magdihttps://innovativehia.com/wp-content/uploads/2020/08/InnovativeHIA_logo2-1030x407.pngmagdi2022-09-11 07:00:142022-08-29 04:34:49Which Industries are Most Susceptible to ACA Penalties from the IRS?

Minimum essential coverage is health insurance that meets the Affordable Care Act requirements. Employers have a requirement to offer at least Minimum Essential Coverage to any benefit-eligible employee. Non-compliance can result in a penalty of $214.17 PER eligible employee per month without coverage.

At Innovative HIA, we aim to offer affordable, flexible, and compliant coverage for all employers.

What Does Minor Medical Cover?

Our Minor Medical plans cover 100% of preventive services and wellness visits to the doctor. In addition, all members have access to 24/7/365 telehealth services and discounts on generic and brand prescriptions.

These plans are the most affordable option under Minimum Essential Coverage.

What Does Major Medical Cover?

Major Medical covers the preventative services and wellness visits mentioned above, as well as primary care and specialist visits with a $15 copay. As well as urgent care, labs, and X-rays with a $50 copay.

24/7/365 telehealth services are included under this plan, along with access to behavioral health telehealth services

Prescriptions under the Major Medical plan are covered based on your coverage tier.

*$50 fee max 3 per year

Preventative Services Covered Under Minor Medical

Both plans cover preventative services and wellness visits. The services covered depend on age and gender. Here’s a look at the coverage offered under preventative services:

Covered Preventative Services for Adults

Abdominal aortic aneurysm one-time screening for men of specified ages who have ever smoked

Alcohol misuse screening and counseling

Aspirin used to prevent cardiovascular disease in men and women of certain ages

Blood pressure screening for all adults

Cholesterol screening for adults of certain ages or at higher risk

Colorectal cancer screening for adults over 50

Depression screening for adults

Diabetes (Type 2) screening for adults with high blood pressure

Diet counseling for adults at higher risk for chronic disease

Falls prevention (with exercise or physical therapy and vitamin D use) for adults 65 years and over

Hepatitis B screening for people at higher risk

Hepatitis C screening for adults at increased risk, and one time for everyone born 1945 –1965

HIV screening for everyone ages 15 to 65, and other ages at increased risk

Immunization vaccines for adults — doses, recommended ages, and recommended populations vary: Hepatitis A, Hepatitis B, Herpes Zoster, Human Papillomavirus, Influenza (flu shot), Measles, Mumps, Rubella, Meningococcal, Pneumococcal, Tetanus, Diphtheria, Pertussis and Varicella

Lung cancer screening for adults 55 – 80 at high risk for lung cancer because they’re heavy smokers or have quit in the past 15 years

Obesity screening and counseling for all adults

Sexually Transmitted Infection (STI) prevention counseling for adults at higher risk

Statin preventive medication for adults 40 to 75 years at higher risk

Syphilis screening for all adults at higher risk

Tobacco use screening for all adults and cessation interventions for tobacco users

Tuberculosis screening for certain adults with symptoms at higher risk

Covered Preventative Services for Women

Anemia screening on a routine basis for pregnant women

Breast Cancer Genetic Test Counseling (BRCA) for women at higher risk for breast cancer (counseling only; not testing)

Breast cancer mammography screenings every 1 to 2 years for women over 40

Breast cancer chemoprevention counseling for women at higher risk

Breastfeeding comprehensive support and counseling from trained providers, and access to breastfeeding supplies, for pregnant and nursing women

Cervical cancer screening

Chlamydia Infection screening for younger women and other women at higher risk

Contraception: Food and Drug Administration-approved contraceptive methods, sterilization procedures, and patient education and counseling, as prescribed by a health care provider for women with reproductive capacity (not including abortifacient drugs). This does not apply to health plans sponsored by certain exempt “religious employers.”

Diabetes screening for women with a history of gestational diabetes who aren’t currently pregnant and who haven’t been diagnosed with type 2 diabetes before

Domestic and interpersonal violence screening and counseling for all women

Folic acid supplements for women who may become pregnant

Gestational diabetes screening for women 24 to 28 weeks pregnant and those at high risk of developing gestational diabetes

Gonorrhea screening for all women at higher risk

Hepatitis B screening for pregnant women at their first prenatal visit

HIV screening and counseling for sexually active women

Human Papillomavirus (HPV) DNA Test every 5 years for women with normal cytology results who are 30 or older

Osteoporosis screening for women over age 60 depending on risk factors

Preeclampsia prevention and screening for pregnant women and follow-up testing for women at higher risk

Rh Incompatibility screening for all pregnant women and follow-up testing for women at higher risk

Sexually transmitted infections counseling for sexually active women

Syphilis screening for all pregnant women or other women at increased risk

Tobacco use screening and interventions for all women, and expanded counseling for pregnant tobacco users

Urinary tract or other infection screening, including urinary incontinence

Well-woman visits to get recommended services for women under 65

Covered Preventative Services for Children

Alcohol and drug use assessments for adolescents

Autism screening for children at 18 and 24 months

Behavioral assessments for children at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Bilirubin concentration screening for newborns

Blood pressure screening for children at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years

Blood screening for newborns

Cervical dysplasia screening for sexually active females

Depression screening for adolescents

Developmental screening for children under age 3

Dyslipidemia screening for children at higher risk of lipid disorders at the following ages: 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Fluoride chemoprevention supplements for children without fluoride in their water source

Fluoride varnish for all infants and children as soon as teeth are present

Gonorrhea preventive medication for the eyes of all newborns

Hearing screening for all newborns, and for children once between 11 and 14 years, once between 15 and 17 years, and once between 18 and 21 years

Height, weight, and Body Mass Index measurements for children at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Hematocrit or hemoglobin screening for all children

Hemoglobinopathies or sickle cell screening for newborns

Hepatitis B screening for adolescents ages 11 to 17 years at high risk

HIV screening for adolescents at higher risk

Hypothyroidism screening for newborns

Immunization vaccines for children from birth to age 18 — doses, recommended ages and recommended populations vary: Diphtheria, Tetanus, Pertussis, Haemophilus influenza type B, Hepatitis A, Hepatitis B, Human Papillomavirus, Inactivated Poliovirus, Influenza (Flu Shot), Measles, Meningococcal, Pneumococcal, Rotavirus and Varicella

Iron supplements for children ages 6 to 12 months at risk for anemia

Lead screening for children at risk of exposure

Maternal depression screening for mothers of infants at 1, 2, 4, and 6-month visits

Medical history for all children throughout development at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Obesity screening and counseling

Oral Health risk assessment for young children Ages: 0 to 11 months, 1 to 4 years, 5 to 10 years.

Phenylketonuria (PKU) screening for this genetic disorder in newborns

Sexually transmitted infection (STI) prevention counseling and screening for adolescents at higher risk

Tuberculin testing for children at higher risk of tuberculosis at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

https://innovativehia.com/wp-content/uploads/2022/07/iStock-961349792-scaled.jpg17072560magdihttps://innovativehia.com/wp-content/uploads/2020/08/InnovativeHIA_logo2-1030x407.pngmagdi2022-07-31 07:00:202022-07-29 18:03:49Preventative Services Covered by Minor Medical

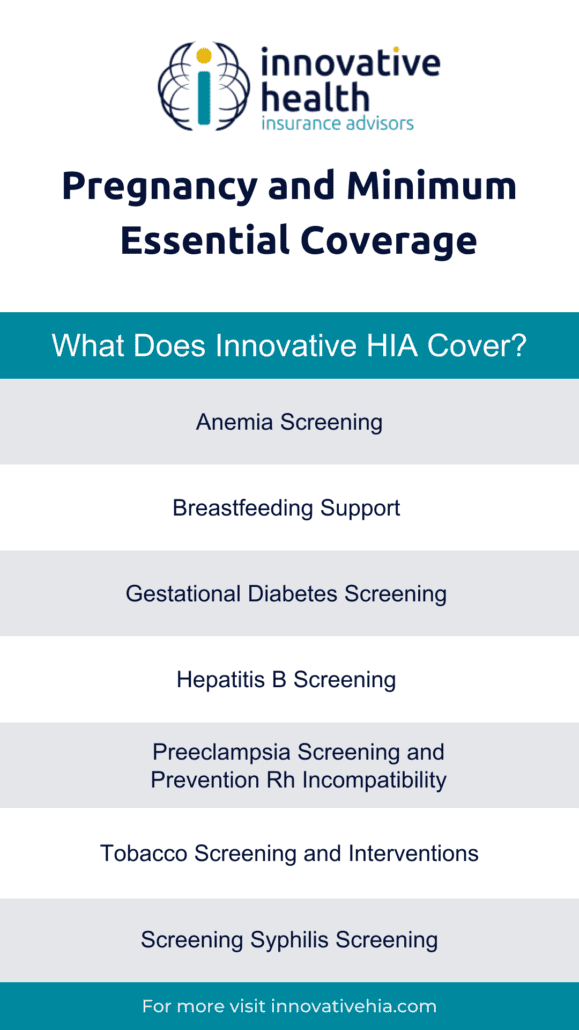

Innovative HIA’s Minor Medical plan (also known as Minimum Essential Coverage) provides expecting mothers the resources to screen for potential risk factors that impact the mother and baby. Some conditions or complications that arise during pregnancy are not easily recognizable and may require screening and testing for a diagnosis. It’s important to routinely check on you and your baby’s health so that if complications arise, your healthcare team is prepared to support your prenatal care. Learn more about pregnancy and minimum essential coverage – what we cover and why it’s important for you and your baby’s health in the short and long term.

What Does Our Minimum Essential Coverage Plan Include for Pregnant Women?

Anemia screening on a routine basis for pregnant women

Breastfeeding comprehensive support and counseling from trained providers, and access to breastfeeding supplies, for pregnant and nursing women

Gestational diabetes screening for women 24 to 28 weeks pregnant and those at risk of developing gestational diabetes

Hepatitis B screening for pregnant women at their first prenatal visit

Preeclampsia prevention and screening for pregnant women and follow-up testing for women at higher risk

Rh Incompatibility screening for all pregnant women and follow-up testing for women at higher risk

Syphilis screening for all pregnant women or other women at increased risk

Tobacco use screening and interventions for all women, and expanded counseling for pregnant tobacco users

What is Anemia?

Anemia is a blood condition where the blood does not have sufficient healthy red blood cells in the body. Red blood cells carry oxygen to your organs and your baby. This means, that reduced levels of red blood cells cause lower levels of oxygen going to your body’s organs and your baby. Symptoms can include fatigue, weakness, and dizziness.

The most common type of anemia during pregnancy is iron-deficient anemia. In iron-deficiency anemia, the blood cells do not have enough iron in them to create sufficient amounts of the protein hemoglobin that carries oxygen itself on the red blood cell.

Therefore, the red blood cells cannot carry as much oxygen to the organs in the body, or the baby. Think of it like a train. The train with six carriages will transport double the amount of people in the same amount of time that a three-carriage train can.

Folate-deficiency anemia occurs when there isn’t enough intake of vitamin folate. Folate is a B vitamin found in food like broccoli and kale. It’s the basis for the body to make healthy red blood cells that can carry oxygen. Maintaining a consistently balanced diet replenishes folate levels in the body.

Vitamin B12 also helps the body create healthy red blood cells. Vitamin B12 deficiency limits the body’s ability to produce healthy red blood cells that circulate enough oxygen to you and your baby. Sources of B12 are found in meat, fish, and dairy products. Again, maintaining a well-balanced diet helps protect you and your baby from potential birth complications.

Why is Screening Important?

When screened for anemia, the test usually includes a hemoglobin test that measures the amount of iron-rich protein in the red blood cells and a hematocrit test that measures the percent of red blood cells in a blood sample.

Severe untreated anemia can lead to pregnancy complications and potentially preterm delivery. We cover anemia screening because we know the importance of catching and monitoring anemia during pregnancy for you and your baby’s safety.

Breastfeeding Support for Pregnant Women

After delivery, one of the first ways to assist women is through breastfeeding support and counseling. Both the American Academy of Pediatrics and the World Health Organization recommend women exclusively breastfeed infants for the first six months.

For women who choose to breastfeed their infant, our Minor Medical plan provides breastfeeding comprehensive support and counseling from trained providers. The support includes access to breastfeeding supplies for pregnant and nursing women.

According to the CDC, “research has shown that breastfeeding is recognized as the best source of nutrition for most infants.”

Breastfeeding counseling encourages and supports mothers during the breastfeeding process. They help the mother:

Correct breastfeeding positioning, attachment, and effective suckling.

Educate the mother on typical feeding behavior such as eating up to eight times a day, and signs such as rooting for when the baby is hungry.

Encourage the mother to switch the breast used after each feeding.

Reassure the mother that she will produce enough milk for her baby.

We encourage the use of trained providers through our Minor Medical benefits to plan to support mother and child during the important feeding process.

What is Gestational Diabetes and Why is Screening Important?

Our Minor Medical benefits plan covers gestational diabetes screening during the second trimester and for women at risk of developing gestational diabetes. During the 24-28 week period, the second trimester of pregnancy, the pregnant woman’s body is more resistant to insulin which makes glucose, sugar, and levels rise. Women who are obese before pregnancy, or have a family history of diabetes, are at a higher risk of gestational diabetes, which makes it important for them to receive screening as well.

Initial glucose challenge test – you drink a sugary solution and your blood is monitored an hour later to check if the levels are normal or out of range.

Follow-up glucose tolerance test – if the first glucose test was high, a second glucose tolerance test is taken. This one requires blood level monitoring every hour for three hours.

It’s important to screen for gestational diabetes so you can prevent any possible future complications. If diagnosed, you and your provider can develop a treatment plan for you and your baby and monitor your health.

Complications for the baby:

Excessive birth weight

Preterm birth

Breathing difficulties

Low blood sugar

Obesity or type 2 diabetes later in life

Stillbirths

Complications for the pregnant woman:

High blood pressure

Preeclampsia

C-section

Future diabetes

Screening for gestational diabetes allows the mother and child to obtain the resources necessary to reduce complications in the future.

In 2010, The Affordable Care Act (ACA), aka Obamacare, was enacted to provide reform to the health insurance industry.

Overall, the Affordable Care Act aimed to accomplish 3 main strategies: make insurance affordable, emphasize prevention, and improve how health care is delivered.

Over a decade later, it’s challenging to ignore the new standards that were derived from the original push to pass this legislation. While the act originally caused disagreements nationwide, there are clear advantages to be noted that have resulted from ACA.

Make Insurance Affordable

The first of the strategies that Obamacare aimed to accomplish was to make health insurance affordable for all Americans.

Oftentimes many assume that they have a clear understanding of the finances of their insurance coverage. However, after landing in the hospital or experiencing a need for emergent care, they would find themselves slapped with high deductibles, unexpected bills, and low maximum coverage. ACA was responsible for making changes to such events.

ACA was able to lower insurance costs for Americans in a variety of ways. The first of which was the provision of tax credits for insurance to middle-class Americans. By limiting out-of-pocket expenses to a maximum of $8,150 for individuals and $17,100 for families, in addition to extending the accessibility of Medicaid beyond 100% poverty level, health insurance became more affordable for many.

In addition to these initial cost caps, ACA allowed parents to keep their children on their medical plans until they reached age 26. It also established the Small Business Health Care Tax Credit, which serves to benefit businesses with less than 25 full-time employees. It provides such businesses with a tax credit that covers up to 50% of their contribution to their employees’ health insurance coverage.

Emphasis on Preventative Care

The second strategy that ACA addressed was putting emphasis on preventive care. Prevention focuses on the promotion of a healthy lifestyle and frequent check-ups to attempt to identify and target potential health issues before they escalate.

The ACA enacted a list of 10 essential benefits that all insurance plans must cover. They include:

Preventive and wellness visits, including chronic disease management

Maternity and newborn care

Mental and behavioral health treatment

Services and devices to help people with injuries, disabilities, or chronic conditions

Diagnostic lab tests

Pediatric dental and vision care

Prescription drugs

Outpatient care

Emergency room services

Hospitalization

In addition to establishing these initial benefit requirements, ACA was responsible for expanding treatment for mental health, addiction, and chronic diseases. From an insurer’s perspective, these are often the most expensive patients for whom to provide ongoing care. ACA put emphasis on programs to combat and prevent this prolonged treatment including those that focus on smoking cessation and combating obesity.

ACA also eliminated lifetime and annual coverage limits and denial of coverage due to pre-existing conditions. Insurance companies are not able to drop or deny you coverage because you have a pre-existing condition, made a mistake on your application, or because you’ve been recently diagnosed with a life-threatening disease. Additionally, they are not allowed to require new members to wait more than 90 days before coverage starts.

Lastly, ACA changed the way that insurers spend premium dollars. It declared that 85% of premium dollars paid by insured members must be spent on healthcare services and quality improvement. If these requirements are not met, insurers are required to provide covered members with a rebate.

Improve Health Care Delivery

The final strategy that Obamacare aimed to tackle was improving how health care is delivered by doctors and hospitals.

One example of such was the establishment of Accountable Care Organizations. Rather than ACA paying for each individual test, procedure, and visit, these organizations were designed to receive coverage payments based on the care and well-being of patients. So far, these organizations have shown significant results. As such, the ACA has continued to encourage them.

Additionally, ACA encouraged the transition to digital medical records. Traditionally, medical records were kept on paper and transferring them required doing so be done by mail or fax. Now, keeping electronic medical records provided a safer, more secure filing system that provided ease of transfer.

ACA also targeted the reduction of fraudulent doctor/supplier relationships. It provided guidance to states reviewing excessive insurance rate hikes and required background checks of all nursing home staff to prevent abuse of seniors.

Overall, the Affordable Care Act, or Obamacare, provided significant advantages to the healthcare industry. The Act was designed to best benefit both insurance suppliers and recipients to ensure that patients in need receive the best care possible without breaking the bank while still ensuring that the insurance industry was not crippled in the process.

While few fully recognize the benefits that were established as a direct result of the Affordable Care Act, many of the implemented changes have since become a recognized standard across the healthcare industry.

Innovative HIA provides a complete solution for ALE employers who want to provide affordable, ACA-compliant benefits to their workers. Our streamlined technology and personal services provide a complete solution for our clients and their employees. Learn more about what we do, here.

https://innovativehia.com/wp-content/uploads/2022/03/Untitled-design-1-copy-3.png9241640Amanda Rogershttps://innovativehia.com/wp-content/uploads/2020/08/InnovativeHIA_logo2-1030x407.pngAmanda Rogers2022-03-11 20:26:462022-03-11 20:26:46What Are the Advantages of the Affordable Care Act?

https://innovativehia.com/wp-content/uploads/2022/01/Untitled-design-copy-6.png9241640Amanda Rogershttps://innovativehia.com/wp-content/uploads/2020/08/InnovativeHIA_logo2-1030x407.pngAmanda Rogers2022-02-13 20:11:322022-04-08 17:41:10Record Number of People Enroll in Health Insurance Coverage

Attention Brokers: Are you offering your ALE clients the most affordable Minor Medical Coverage (MEC)? How can you offer your applicable large employers a one-stop shop for all their needs? Benefits are no longer about simply meeting Minimum Essential Coverage options. You need to offer worksite and voluntary benefits, telehealth options, call center availability, and easy portal management. Why should you offer these options to your employers? Because they want them.

In order for employers to attract and retain great talent, they need great benefit options. This means going beyond standard Minor Medical requirements and offering services that provide value and attract the best workers.

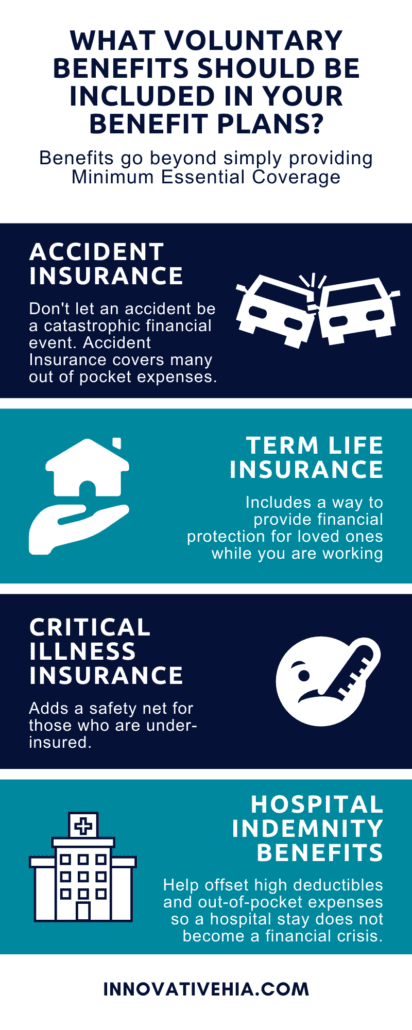

Let’s Start with Voluntary Benefits

Worksite and voluntary benefits include accident insurance, term life insurance, critical illness insurance, and hospital indemnity.

Accident insurance includes aid in payment for medical and out-of-pocket expenses that may occur due to an accident occurring.

Term life insurance includes a way to provide financial protection for loved ones while employees are working.

Critical illness insurance adds a safety net for those who are under-insured.

Hospital indemnity benefits help to offset high deductibles and out-of-pocket expenses so a hospital stay does not become a financial crisis.

Next, Consider Offering Your Employees Access to Telehealth Care

With 24/7 access to doctors, telehealth–also known as Virtual Health–can help employees get care when they need it with added convenience. At Innovative HIA, we offer telehealth options that include behavioral health and therapy access, to give employees the ability to speak to a therapist whenever they need it.* In addition, it helps employees receive necessary prescriptions without having to go to a doctor’s office.

Employers look for convenience when looking for benefits, as a broker you can provide a one-stop-shop for all your ALEs benefits needs. This means 24/7 call center support and easy access to portal management, single-point billing, and US-based customer care.

At Innovative HIA, we offer portal management access to provide employers with the ability to make plan changes, order ID cards, and have them shipped within a few days, check their claim statuses, and give employees the ability to manage their own profiles.

With bilingual call center support, you’re getting licensed representatives to help manage enrollment and provide year-round support. All of our representatives are in-house, which means they understand your client’s needs.

Innovative HIA can provide a one-stop shop for all employers to handle their benefit needs. As a broker, it is your responsibility to provide your employers with the best possible options for their needs. Contact us to learn more!

https://innovativehia.com/wp-content/uploads/2022/02/Untitled-design-copy-4.png9241640Amanda Rogershttps://innovativehia.com/wp-content/uploads/2020/08/InnovativeHIA_logo2-1030x407.pngAmanda Rogers2022-02-11 18:37:382022-06-03 19:54:39Attention Brokers: Are You Offering Your ALE Clients the Most Affordable MEC?

https://innovativehia.com/wp-content/uploads/2022/01/Untitled-design-copy-4.png9241640Amanda Rogershttps://innovativehia.com/wp-content/uploads/2020/08/InnovativeHIA_logo2-1030x407.pngAmanda Rogers2022-02-06 19:27:272022-01-27 19:45:07What is Minor Medical and What Does It Cover?

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.